Customers expect a seamless transition between their digital and in-person banking experiences. For example, they might want to start a mortgage application online and finish it (quickly) in person — all with tech that works together.

Banking leaders know they need to update their physical spaces, and they’re investing to give customers a great experience. Thirty-five percent of financial institutions planned to expand their branch networks in 2025, climbing to 61% among credit unions.[1]

But while half of financial institutions call digital experience their top priority, only about a quarter are modernizing the legacy systems that actually make those experiences work.[2] Rather than software, the gap is often due to the hardware at the counter.

Smart bankers are looking to invest where it matters — the devices that connect it all.

Paper checks are still very much in the picture — and so is check fraud

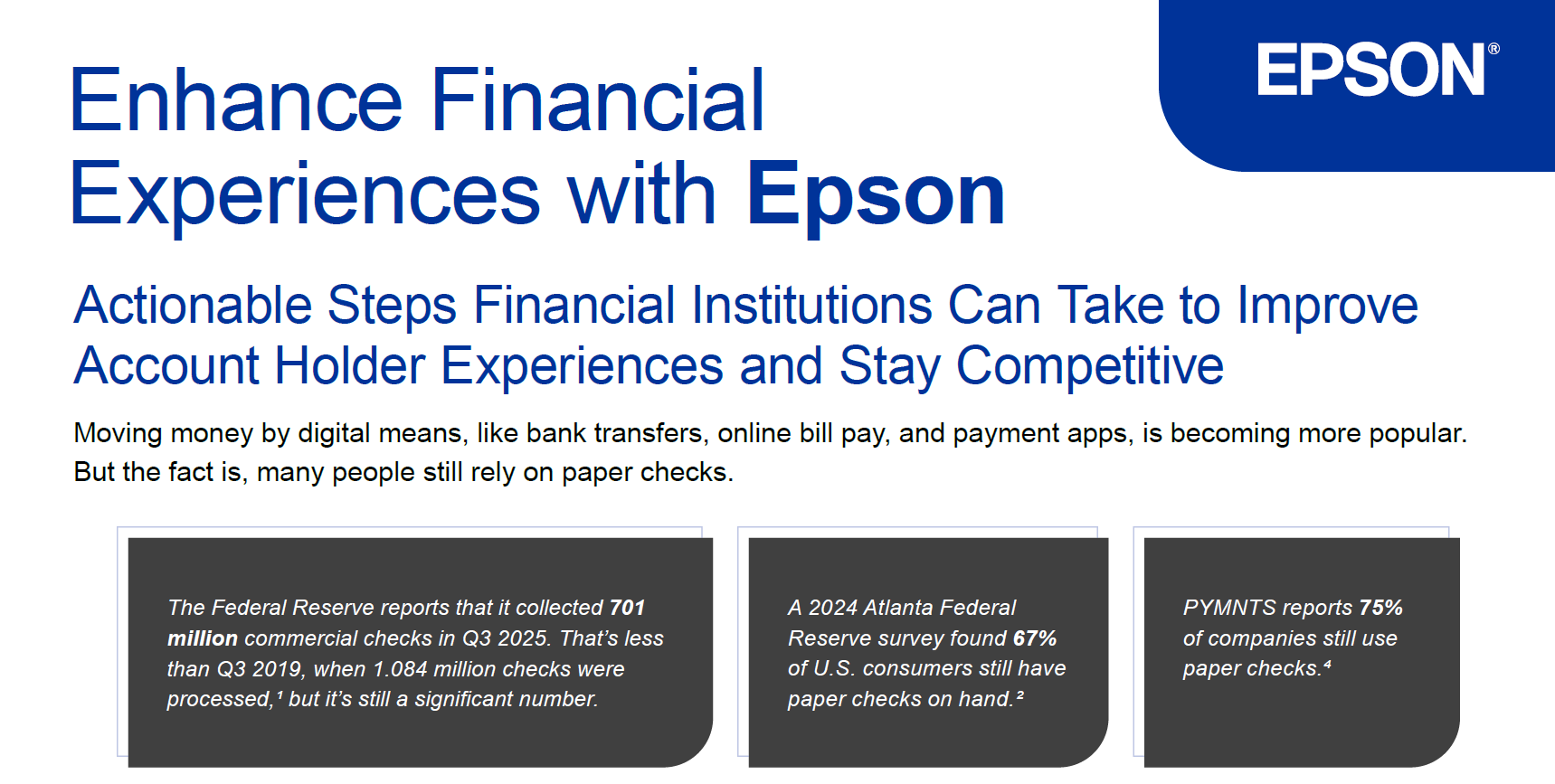

Any conversation about branch hardware must address the role of checks. The Federal Reserve processed 701 million commercial checks in Q3 2025 — down from 1.084 billion in Q3 2019, but hardly a rounding error.[3] Three in four companies are still writing checks,[4] and Mastercard puts checks at more than half of the $25 trillion B2B payments market.[5]

There’s a convenience-driven inertia with checks. You can write a check to anyone without requiring them to download an app, it creates automatic proof of payment, and most institutions don’t charge for processing. Volumes will keep shrinking, but the last check won’t be written for a long time.

That volume creates a fraud surface. FinCEN reported more than 680,000 check-related Suspicious Activity Reports in 2022, nearly double the 2020 count.[6] The crime is sixties-era low-tech, with checks stolen from mailboxes and ink washed off, but every dollar of fraud loss costs $4.36 by the time it’s resolved.[7] So scanning speed becomes a security question, not just an efficiency one.

Click here or the image below to view an informative infographic about the steps banks and financial institutions can take to improve customer experiences.

Integrated hardware as the connective tissue

The multifunction teller device brings new efficiencies to the processing of checks. One compact unit handles check scanning, two-sided ID capture, endorsement printing, receipt printing, and magnetic stripe reading, without the teller having to swivel between separate machines. Epson’s TM-S9000II-NW and TM-S2000II-NW offer integrated two-sided ID card scanning. Both scan checks at up to 225 documents per minute over USB (200 via network), feed through a 100-check document hopper, and connect via USB 2.0 and Ethernet with multi-platform support.[8] The Epson TM-S9000II-NW also adds a built-in thermal receipt printer, so there’s one less device at the counter.[9] Pair the TM-S2000II-NW with Epson’s OmniLink TM-T88VII thermal receipt printer (500 mm/sec print speed) and you get the same capability as a separate station.[10]

The teller counter is also ground zero for dealing with fraud. Built-in ID scanners and optional magnetic stripe readers feed identity data directly into fraud-detection tools at the point of interaction, which matters when 60% of financial institutions reported rising fraud in 2025.[11] The OmniLink receipt printer adds a data layer too, collecting transactional information in real time that can be compared across customer demographics for pattern detection.[12] That’s useful both for flagging suspicious activity and for identifying staffing or upselling opportunities.

From the teller counter to the client’s doorstep

The value of a well-integrated hardware foundation extends outward from the counter into the lobby, across town, and into the field.

Mortgage originations grew by $512 billion in Q3 2025,[13] and RFI Global found that people in more than half of U.S. households still visit their branch, with 37% talking to a teller for routine transactions monthly.[14] Each of those visits is a chance to turn a compliance step into a real conversation.

At the counter, hybrid account opening helps a customer who began a mortgage application online and comes in to verify her identity and sign. The multifunction device scans both sides of her ID, reads the magnetic stripe, and endorses documents. Because it’s networked, the online application data is already available, so no re-entry is needed. Move to the lobby, and self-service kiosks combine check deposit, ID verification, and receipt printing in a single station. A customer in a modernized branch can handle a routine deposit and walk out with a printed confirmation, all without waiting for a teller. Routine deposits shift to the kiosk. Staff shifts to the advisory conversations that actually generate revenue.

Move further to the client’s location. Small businesses with heavy check volume can use the Epson TM-S1000II-NW, a driverless desktop scanner with Ethernet, USB, and optional Wi-Fi,[15] to scan checks and deposit electronically. Magnetic ink character recognition provides secure processing with no trip to the bank, and deposits are processed at any hour.

Field agents with wireless receipt printers and tablets can also open accounts and process deposits at pop-up events, college orientations, or a client’s office. Even inside the branch, that same mobility lets a representative meet a customer at any scanner station for a check-only deposit, so nobody stands in line for a 90-second transaction.

For the heavier paperwork such as loan applications and account-opening documentation, Epson’s DS-790WN document scanner runs at 45 pages per minute with one-pass duplex and wireless networking.[16] So, scanned documents become accessible from any branch. Epson is your partner in financial services scanning. Keypoint Intelligence named Epson its 2025 Scanner Line of the Year.[17]

Buying hardware that won’t be obsolete in three years

None of this works if today’s equipment can’t adapt to tomorrow’s network. Devices offering USB 2.0, Ethernet, and Wi-Fi give institutions room to migrate architectures without ripping out hardware. Driverless scanners go further, plugging into new software environments without compatibility headaches. Multi-platform support matters especially after mergers, when a single institution might be running three different core banking systems across its branch network.

Our mortgage customer’s visit went smoothly because the ID scanner communicated with the application system, the receipt printer confirmed the transaction on the spot, and no one asked her to repeat what she’d already entered on her laptop three days earlier. No futuristic technology made that happen. Just the right devices, connected and thoughtfully placed.

The hardware layer will play a key role as branches evolve from transaction processing centers into advisory hubs. Visit https://epson.com/financial-point-of-sale-solutions for more information about how Epson can help.

[1] “Banks Struggling to Navigate the 2025 Retail Banking Landscape.” The Financial Brand, ‘2025 Retail Banking Trends and Priorities’, May 5, 2025, thefinancialbrand.com/news/banking-trends-strategies/competitive-pressures-are-scrambling-retail-banks-priorities-in-2025-188842

[2] “2025 Retail Banking Trends and Priorities.” Digital Banking Report, ‘2025 Retail Banking Trends and Priorities’, Mar 12, 2025, www.digitalbankingreport.com/trends/2025-retail-banking-trends-and-priorities/

[3] “Federal Reserve Board – Commercial Checks Collected through the Federal Reserve–Quarterly Data.” Board of Governors of the Federal Reserve, ‘Commercial Checks Collected through the Federal Reserve – Quarterly Data’, www.federalreserve.gov/paymentsystems/checkcommcheckcolqtr.htm

[4] “75% of Companies Still Use Paper Checks Despite High Cost.” PYMNTS, ‘Getting Paid: Digital Payments for Improving Cash Flow and Customer Experience,’ August 2024, Aug 29, 2024, www.pymnts.com/digital-payments/2024/75percent-companies-still-use-paper-checks-despite-high-cost/

[5] Mastercard, “How Industry 4.0 is defining the future of business payments”, https://www.mastercard.us/content/dam/public/mastercardcom/na/us/en/documents/business-payments-2022-whitepaper.pdf

[6] FinCEN, “FinCEN Alert on Nationwide Surge in Mail Theft-Related Check Fraud Schemes Targeting the U.S. Mail”, February 2023, https://www.fincen.gov/news/news-releases/fincen-alert-nationwide-surge-mail-theft-related-check-fraud-schemes-targeting

[7] LexisNexis, “Annual LexisNexis Risk Solutions Report Finds Fraud Costs up to 22.4% from Pre-Pandemic Levels Across U.S. and Canadian Financial Services Firms”, Nov 2022. https://www.prnewswire.com/news-releases/annual-lexisnexis-risk-solutions-report-finds-fraud-costs-up-to-22-4-from-pre-pandemic-levels-across-us-and-canadian-financial-services-firms-301675103.html

[8] “Epson to Showcase Leading Solutions at the Financial Brand Forum 2025 | Epson US.” Epson, Financial Brand Forum 2025 press release, news.epson.com/news/check-scanners-POS-financial-brand-forum-2025

[9] “Epson TM-S9000II-NW Network Multifunction Teller Device | Products | Epson US.” Epson, TM-S9000II-NW product page, epson.com/For-Work/Scanners/Check-Scanners/Epson-TM-S9000II-NW-Network-Multifunction-Teller-Device/p/A41CK43031

[10] “OmniLink TM-T88VII Single-station Thermal Receipt Printer | Products | Epson US.” Epson, OmniLink TM-T88VII product page, epson.com/For-Work/POS-System-Devices/POS-Printers/OmniLink-TM-T88VII-Single-station-Thermal-Receipt-Printer/p/C31CJ57052

[11] “Alloy’s 2025 State of Fraud Report.” Alloy, ‘2025 State of Fraud Report’, www.alloy.com/reports/fraud-report-2025

[12] “Whitepaper – The Evolution of Branch Banking | Epson US.” Epson, ‘Branch of the Future’ whitepaper, epson.com/whitepaper-banking-branch-of-the-future

[13] “Household Debt Balances Grow Steadily; Mortgage Originations Tick Up in Third Quarter.” Federal Reserve Bank of New York, ‘Household Debt and Credit Report, Q3 2025’, www.newyorkfed.org/newsevents/news/research/2025/20251105

[14] “Why bank branches still matter: generational insights.” RFI Global, ‘Why bank branches still matter: Generational insights from Boomers to Gen Z,’ October 2025, Oct 13, 2025, rfi.global/why-bank-branches-still-matter-generational-insights-from-boomers-to-gen-z/

[15] “Epson to Showcase Leading Solutions at the Financial Brand Forum 2025 | Epson US.” Epson, Financial Brand Forum 2025 press release, news.epson.com/news/check-scanners-POS-financial-brand-forum-2025

[16] “Epson DS-790WN Wireless Network Color Document Scanner | Products | Epson US.” Epson, DS-790WN product page, epson.com/For-Work/Scanners/Document-Scanners/Epson-DS-790WN-Wireless-Network-Color-Document-Scanner/p/B11B265201

[17] “Epson is Named 2025 Scanner Line of the Year by Keypoint Intelligence.” Keypoint Intelligence, ‘2025 Scanner Line of the Year’, Feb 20, 2025, www.prnewswire.com/news-releases/epson-is-named-2025-scanner-line-of-the-year-by-keypoint-intelligence-302380570.html

![]()